All topics

Can active investing make a comeback?

Looking over S&P Dow Jones Indices’ most recent SPIVA score cards, the outlook for active managers – overall – appears to be quite dire. These SPIVA score cards measure actively managed funds against their index benchmarks worldwide. Broadly speaking, most active investors fall short of benchmark performance.

This has led some commentators to argue that simply hugging an index, like the S&P 500 or the FTSE 100, is a much better (meaning cheaper) way of getting exposure to possible positive returns from different equity opportunity sets. Similar points have been made regarding fixed income products and other asset classes.

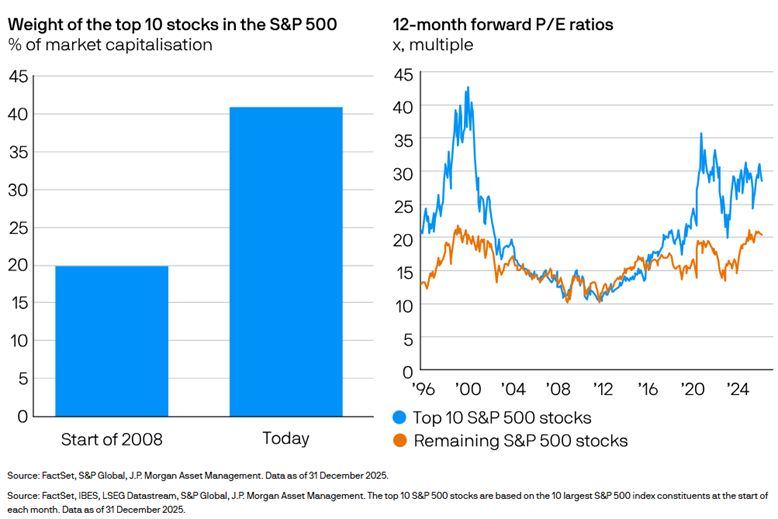

Over the last 50 years, passive investing has continued to grow, in part due to the underperformance of active managers. This developed is, however, not without risks. For example, JP Morgan Asset Management argues that: “While 20 years ago, a passive approach provided well diversified exposure, the same is clearly not true today.”

As such, the question remains: Does active investing still play a role in today’s markets? Let’s take U.S. equity managers as a case study in attempting to answer this question.

The fate of U.S. equity managers

In the U.S., looking at the relative performance of equity managers, there are high rates of underperformance among large-cap, mid-cap, as well as small-cap managers.

The SPIVA report reads:

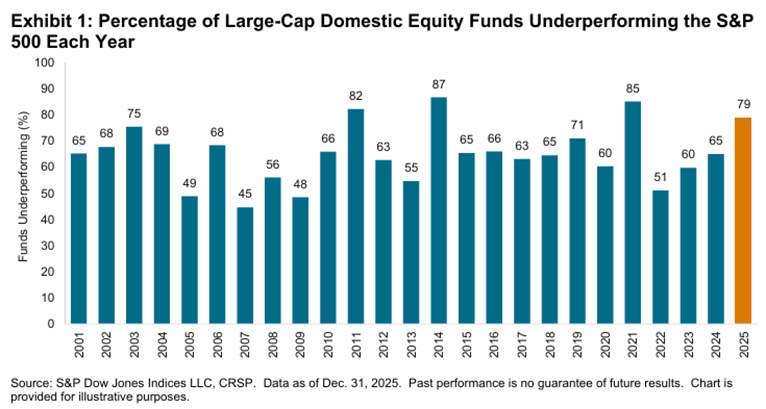

“In our largest and most closely watched comparison, 79% of all active large-cap U.S. equity funds underperformed the S&P 500, worse than the 65% rate observed in 2024 and the fourth-worst year for active large-cap managers over the 25-year history of our SPIVA Scorecards. […] 55% of all mid-cap funds and 41% of all small-cap funds underperformed.”

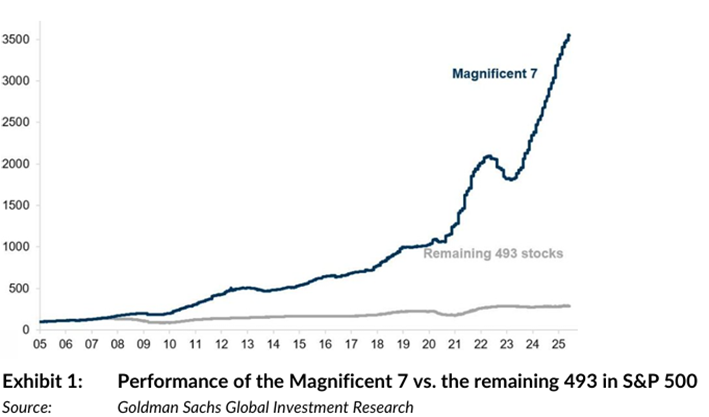

We can already see that U.S. small-cap equity managers, broadly speaking, fared better than those seeking alpha among mid-cap or large-cap stocks. One of the reasons for this has been the growing concentration of the U.S. stock market’s performance in a handful of stocks, particularly within the technology sector.

Although this risk is not new, as Elm Partners argues, it has increased in recent years as passive flows have followed the winning technology stocks, seen as strong plays on artificial intelligence (AI). The danger here is that this trend can reverse itself, leading to massive underperformance of index-hugging strategies. As this piece from Absolute Return Partners points out: “From peak to trough in the dotcom bust in 2000-02, the Nasdaq Composite index declined by no less than 77%. You should never assume that this can’t happen again.”

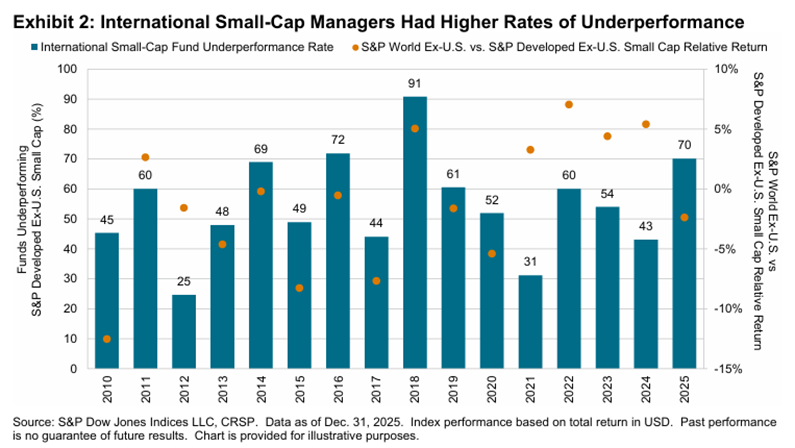

Is the situation for European equity managers different, however? Over the last few months, there has been much talk of the ongoing rotation away from U.S. markets, especially stocks, towards international opportunities. However, ex-U.S. equity managers have also had a difficult time overperforming their benchmarks, especially those focused on small-cap equities.

Indeed, one of the regions that was seen as benefiting from these capital flows moving away from the U.S. was Europe. The situation there, however, is not much different: active equity managers, broadly speaking, failed to keep up with their benchmarks, according to the latest SPIVA data.

Does this mean that passive investing is the only solution to achieve consistently high stock market returns? The growth of this part of the financial system would answer this question in affirmative. However, there are caveats (one of them was mentioned above and enforced by the chart below).

Passive investing has grown. Can it continue to do so?

The growth of passive strategies is not a story that is unknown. Passive equity strategies have reached c. $20trn in 2024, according to a paper by Apollo. Behind this growth story is one word: economics.

Passive investment products are much cheaper than actively managed ones. When this consideration is put side by side with the large number of underperforming active managers, the proposition offered by passive investment products can be quite attractive.

However, the reality is a bit more complex, as Natixis Investment Managers explained:

“The rise of passive investing is indisputable, and the economic arguments underpinning it cannot be contested. However, an investor must not confuse the logic behind choosing to invest passively with a risk free or impact free alternative. On the contrary, given its size today and its construction anchored on company capitalization and past momentum, the implicit cost of passive growth today is multifaceted, disrupting market balance and elasticity far beyond what its name might suggest.”

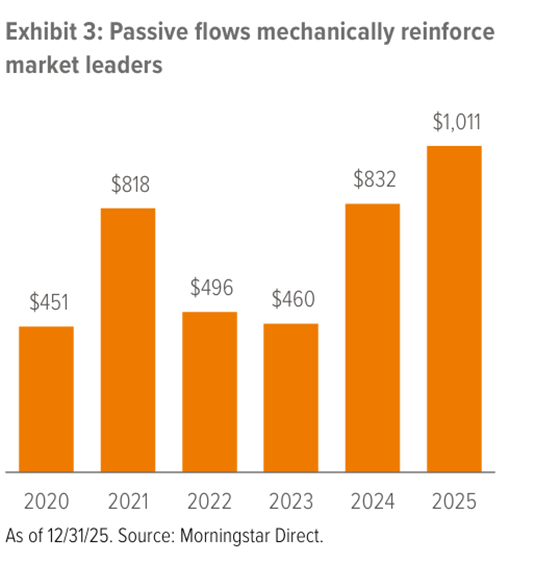

As the chart below from Voya Investment Management illustrates, passive flows reinforce market leaders, leading to more momentum and market concentration, which results in a riskier proposition for passive investors.

Alliance Bernstein put it so:

“[…] the passive index is riskier than it has been in the past. The confluence of high concentration, a dominant factor driving returns (in the sense of a principal component analysis), and high valuations points to the idea that there is complacency about volatility today. The scale of the flows that have been disproportionately into passive cap-weighted funds with a high exposure to the mega cap companies implies the risk of a significant negative wealth effect if there is an upset to expectations for those large companies.”

As such, the answer to the question above seems to be this: Passive strategies will grow if their buyers think the risk is low. However, perception and reality may – and, indeed, they often do – differ.

What does this mean for allocators today

Let’s hear from some active managers their views on what investors should do in this complex environment.

MFS: “We believe this is where active management can help most: using evidence to separate durable business models from those facing true AI-driven erosion.”

Robeco: “Understanding the underlying risk exposures in portfolios, and assessing returns on a risk-adjusted basis, is essential for meaningful manager comparison and portfolio construction.”

Fidelity International: “[…] active asset allocation remains crucial for managing the challenges and opportunities presented by abrupt changes to conditions and higher volatility.”

RELATED CONTENT

Why U.S. Sectors Matter to Europe (S&P Dow Jones Indices)

| 29 Jul 2026During the first quarter, energy stocks had an outsized effect on the broader market as oil supply shortages, fueled by the war in Iran, rippled…

Real Estate: International Diversification for U.S. Investors (PGIM)

| 29 Jul 2026The United States is an outperformer in today’s global real estate market, but a combination of heightened market risks and portfolio-level factors…

Private Credit Defaults, Recoveries and AI Risk (Nuveen)

| 29 Jul 2026Explore Nuveen's latest Private Capital Call episode featuring KBRA's Chief Rating Officer, Bill Cox, and Head of Default Research, Eric…

Global Investment Views - August 2026 (Amundi)

| 29 Jul 2026July saw tensions flare once again in the Middle East. Markets questioned the feasibility of returning to a ceasefire, pushing Brent oil prices back…

Finding Opportunity in Real Estate (PGIM)

| 29 Jul 2026On the No Cap podcast, Soultana Reigle, Head of U.S. Equity and Senior Portfolio Manager for U.S. Value-Add Strategies, discusses where PGIM is…